Apollo Limits Investor Withdrawals Amid Surge in Redemption Requests

1-Minute Brief

Investor concerns over private credit exposure have led to heightened redemption requests and partial payouts at major funds.

Key Facts

- Apollo honored only 45% of investor withdrawal requests from its $15 billion private credit fund in the latest quarter.

- MarketWatch reports that a repeat of 2008-level private credit defaults would reduce GDP growth by between one-fifth and one-half of a percentage point.

- Apollo's fund experienced a surge in redemptions similar to trends seen at rival private credit firms.

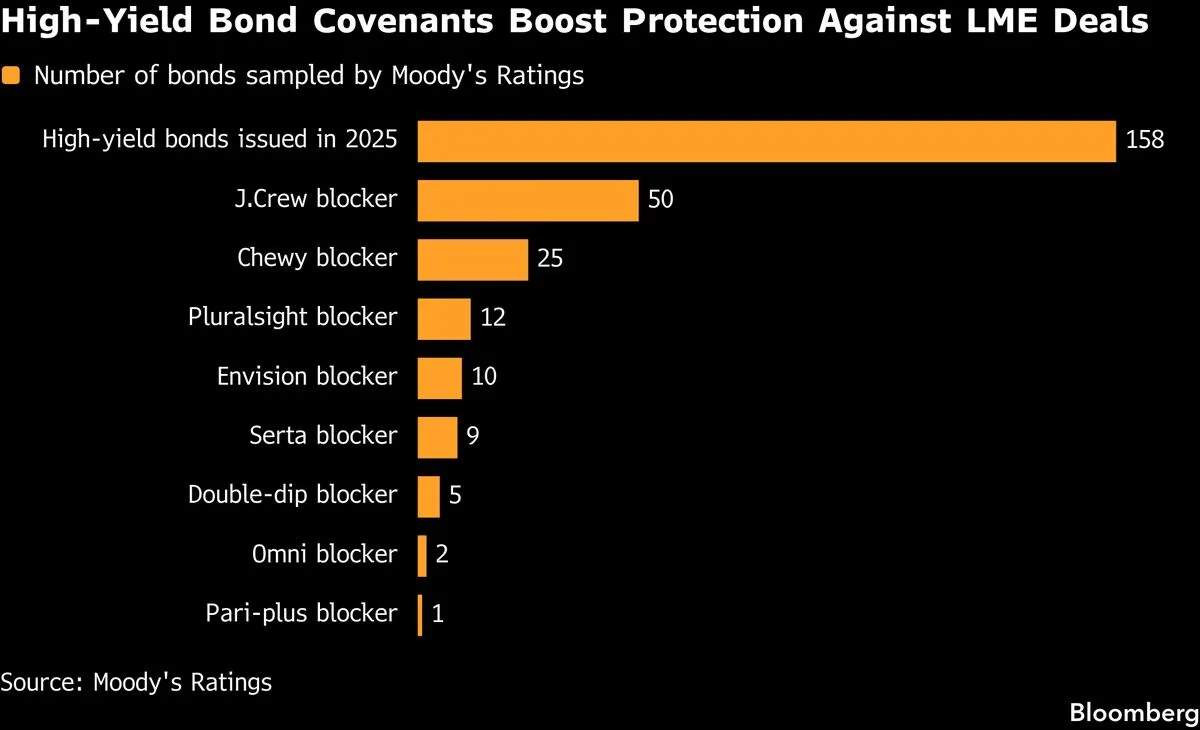

- Junk bondholders are increasingly resisting aggressive asset transfers by borrowers, a practice referred to as 'pulling a J. Crew'.

- Apollo's stock price declined following the announcement of limited redemptions.

What Happened

Apollo Global Management limited investor withdrawals from its $15 billion private credit fund, fulfilling only 45% of redemption requests in the latest quarter amid increased investor demand for liquidity.

Why It Matters

The move reflects broader investor unease about private credit exposure and signals potential stress in the sector, which could have implications for financial markets and economic growth.

What's Next

Market participants are watching for further redemption restrictions and monitoring the impact of potential private credit defaults on the broader economy.

Sources

Confirmed by 3 independent sources

- CNBCCenter20h agoApollo gives investors only 45% of requested withdrawals from $15 billion private credit fund

- Bloomberg MarketsCenter4h agoJunk Bond Buyers Are Increasingly Refusing To Be ‘J. Crewed’

- MarketWatchCenter9h agoHow the economy would weather private-credit defaults rising to financial crisis-like levels